Tracking Error

Later this quarter (Q1 2022), First Ascent will be introducing a direct indexing offering to the advisors we work with. We call our new offering Customized Index Portfolios.

Customized Index Portfolios hold individual stocks and can be designed to reflect the investment goals, values, and preferences of clients with $250,000 or more to invest.

In anticipation of the launch of our Customized Index Portfolios, we are providing a detailed explanation of the term “tracking error,” since it is a term that comes up often in discussions about direct indexing portfolios. Here’s our take on the concept of “tracking error.”

What Is Tracking Error

Tracking error measures the variation in performance between a portfolio and its benchmark.

The main cause of tracking error is the difference in the holdings of the portfolio and the benchmark. Typically, the greater the difference in holdings, the greater the tracking error.

Tracking error is usually calculated as the standard deviation of the difference in the returns of the portfolio and its benchmark. This may sound complicated, but it is simply a way to measure the variation in returns between the portfolio and its benchmark over time.

Here’s an example. Let’s compare the performance and tracking error of two ETFs that both use the S&P 500 Index as their benchmark but construct their portfolios in different ways.

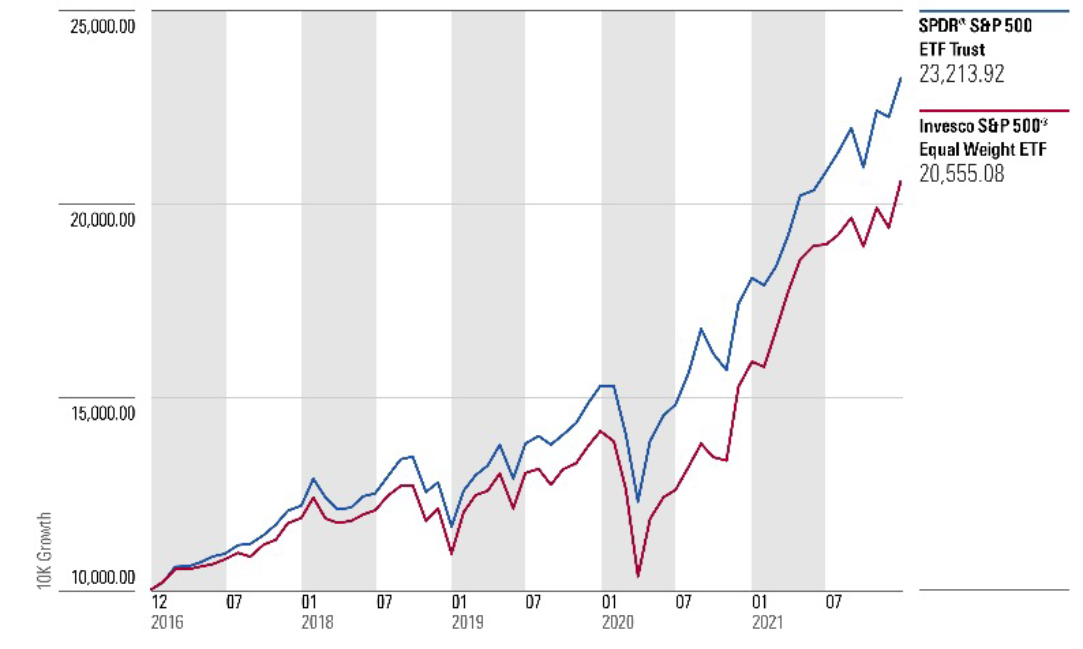

The SPDR® S&P 500 ETF Trust (SPY) is designed to closely track the performance of the S&P 500 Index. The S&P is a “capitalization-weighted” index, so stocks with larger market capitalizations are weighted more heavily than stocks with smaller market capitalizations. As a result, with only minor deviations, SPY holds the same stocks as the S&P 500 in the same weights.

The Invesco S&P 500 Equal Weight ETF (RSP) uses an “equal-weighted” approach to portfolio construction. Stocks in the portfolio are weighted equally, rather than based on their market capitalizations. While RSP holds all the same stocks as the S&P 500, the weightings of those stocks in the portfolio can vary meaningfully.

Because of the differences in the ways SPY and RSP are constructed, we would expect to see differences in both their performance and their tracking error relative to their benchmark, the S&P 500 Index. And, in fact, that is what we see.

The graphic below shows that SPY outperformed RSP for the period 2017 through 2021. SPY generated an annualized return of 18.33%. RSP generated an annualized return of 15.48%.

Growth: SPY vs. RSP

Last 5 Years

Data Source: Morningstar

The differences in portfolio construction between SPY and RSP also show up in their tracking errors. Since SPY is constructed very similarly to its benchmark, its tracking error is very low, 0.04. RSP is constructed differently than its benchmark, so its tracking error is higher, 4.89.

Differences in tracking error also show up as stocks are eliminated from a portfolio based on environmental, social, or governance issues. Again, this happens because the holdings of the portfolio and its benchmark become increasingly dissimilar as more stocks are eliminated.

Here’s an example. SPY, which, as we saw, closely tracks the S&P 500 Index, has a not-so-distant cousin, SPDR® 500 Fossil Fuel Reserves Free ETF (SPYX). SPYX is constructed similarly, but eliminates stocks of certain companies involved in the fossil fuel industry.

Over the same 2017 through 2021 period, SPYX had an annualized return of 18.98% compared to 18.33% for SPY. As SPYX’s holdings vary more from the S&P 500 Index than SPY’s holdings, its tracking error is slightly higher at 0.67, compared to 0.04 for SPY.

Growth: SPY vs. SPYX

Last 5 Years

Data Source: Morningstar

The same is true if a portfolio is tax managed. If a portfolio is designed to track an index, but stocks are bought and sold during the year to generate tax losses, tracking error will increase. That is because the holdings of the portfolio and the index will vary as tax losses are harvested.

There is no such thing as a “typical” or “appropriate” amount of tracking error. The acceptable level of tracking error is determined by each investor.

Tracking error is neither good, nor bad. The performance of a portfolio with a 1.0 tracking error to its benchmark can be either higher or lower than the performance of the benchmark. But investors should be aware that they will experience greater tracking error the more the holdings in their portfolios vary from the holdings of the indexes they are trying to track.